If we legalize recreational cannabis, in any jurisdiction, at what rate will it be taxed? How will these new dollars be used? Each state contemplating legalization of recreational cannabis faces this question, and faces a unique opportunity to develop regulations that ensure the needs of its populace are being met.

Already, different policies are being implemented from one jurisdiction to the next.

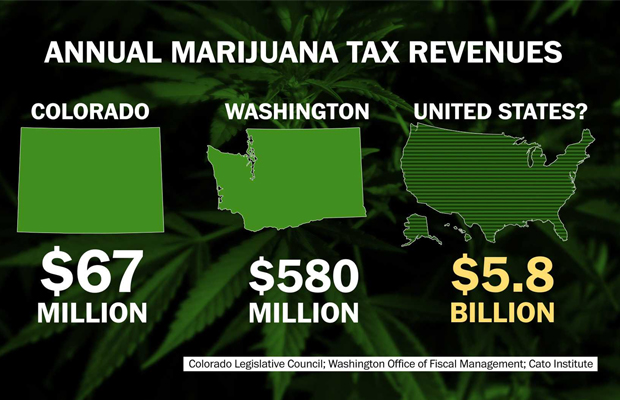

In Colorado, medical marijuana users pay the state 2.9 percent and any additional local sales tax, whereas recreational users pay an extra 10 percent to the state. The sales tax revenue goes directly to the state, and local taxes go to local jurisdictions.

In the state of Washington, sales of recreational and medical cannabis are both subject to sales tax. Medical cannabis is exempted from “the retail sales tax exemption provided for prescription drugs, but only when prescribed as authorized by the laws of this state”.

Because cannabis is a Schedule I controlled substance, cannabis is recommended rather than prescribed. Additionally, retail sales of recreational cannabis are subject to business and occupation tax; a partial or complete credit towards this tax only is available for medical cannabis sellers. Here, too, sales tax revenue goes directly to the state.

One of the main benefits of legalizing recreational cannabis is the fiscal benefit to the state. I propose that some of the additional taxes collected be redirected and put towards covering medical cannabis costs for those who need but cannot afford it.

Additionally, some dollars need to go to community health, education, research, harm reduction and drug and alcohol rehabilitation programs to help balance the impact of the implementation of recreational cannabis laws. We do face a challenge in defining these categories of need and affordability, particularly in the context of medical cannabis.

At minimum, using some of the additional revenue created by legalizing recreational cannabis could be routed towards covering sales tax on medical cannabis. Alternatively, a clinical protocol (based on the ICD-9?) could be implemented alongside subsidization of costs for those who qualify based on participation in low-income government programs or an alternative metric.

In January, Colorado made $2 million in tax revenue from the sales of recreational cannabis. This can only be the tip of the fiscal iceberg for this industry; we must consider where these new dollars will go as we ponder legalization in each jurisdiction.

Do you agree with Alexandra? Should recreational tax revenues subsidize medical users? Tell us in the comments below!