Economics

25% Less Cannabis Brands on California Shelves Since Legalization

The new July point-of-sale data from BDS Analytics illustrates the short-term consequences of California’s adult-use cannabis regulations since Jan. 1, 2018. For example, there are 16 percent fewer cannabis brands on dispensary shelves since July 1.

Since California’s legal adult-use cannabis market came online on Jan. 1 and new testing and packaging regulations were enforced on July 1, the state’s legal cannabis industry has struggled through regulatory hoops or local roadblocks. According to new data, these growing pains have a consequence: There are now 25 percent fewer cannabis brands on dispensary shelves in California than there were in December 2017.

The data comes from the Colorado-based company BDS Analytics, who released their calculations from July’s point-of-sale numbers this week.

“California is going to have three extinction-level events,” BDS Analytics California Regional Director Tamar Maritz told Cannabis Now, following the release of the new numbers.

She said the first “extinction-level event” was the turn of the year, the second was on July 1 and the third will be with the forthcoming implementation of the state’s track-and-trace system.

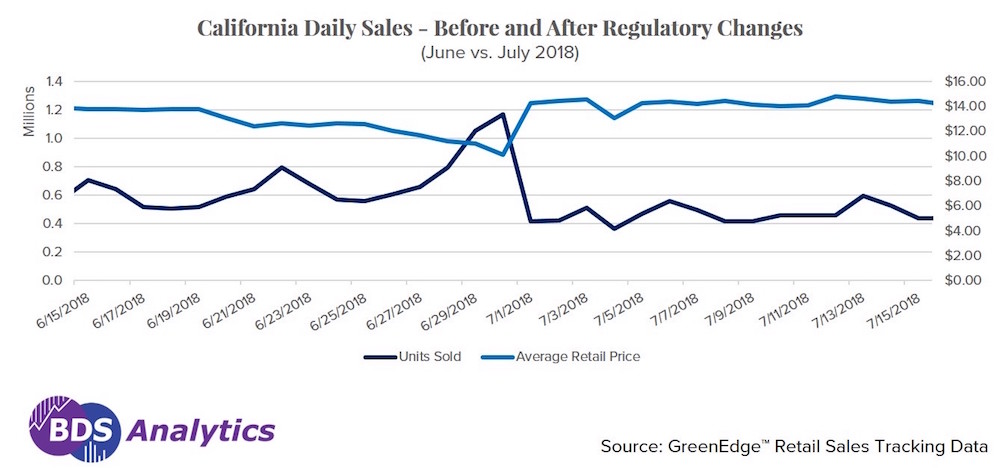

From June to July of this year, total sales volume dropped 13 percent.

One of the most interesting things about the July point-of-sale data from BDS Analytics is that it’s clear the market recognized exactly what was coming on July 1. The last two days of June saw a 30 percent higher volume of sales than any month previously tracked, according to BDS. Dispensary customers were essentially taking advantage of some of the greatest deals ever as retailers attempted to offload as much flower as they could that didn’t meet the new testing standards.

The June sales record for California’s legal market was matched with a record for the cheapest marijuana prices ever in most cases, providing a clear example of the basic economic principle of supply and demand. You can see the numbers actually flip for a few days visually in graphics created by BDS Analytics.

BDS Analytics works with numerous dispensaries to get hard numbers from point of sale systems to acquire its GreenEdge data. That’s also where they acquire all of the numbers to establish top brands.

16% Fewer Brands on Dispensary Shelves Since July 1

Beyond sales numbers, July saw a significant decrease in the number of brands actually available on shelves. BDS Analytics tracked the barcodes of 400 brands in June, by the end of July, that number had dipped to 336. This means 64 brands didn’t meet demands or simply were discontinued for other reasons.

The biggest dips in the number of brands available have coincided with regulatory implementation both times. On the eve of legal marijuana sales in California, 452 brands were being tracked across the marketplace, according to BDS Analytics. In January, that number dropped significantly to 338 brands. The number of brands available trended downward for a few months, and then in May and June, the count got back up to 400 brands.

With the July dip, the total number of brands compared to December is down a little under 26 percent. However, BDS Analytics projects that the number of brands available will recover and climb back up again in the months to come.

“Right now you’re seeing an upward trajectory,” Maritz said.

While these numbers reflect the segment of the market covered by BDS Analytics, various pictures of empty shelves all over the place emerged at the beginning of July. It’s not unreasonable to presume distributors outside the data pool were hit with similar realities to the ones covered by BDS Analytics.

However, despite all this fluctuation, experts are still predicting the market is still poised to explode in the next few years and that the current turbulence is just the hiccups of the emerging market. As BDS’s June report in collaboration with ArcView Market Research noted, the cannabis industry is still poised to triple in size by 2022 to a value of $32 billion. Due to the restrictions of the US market is will expand 5.2 percent slower than other markets across the globe, the report predicted.

TELL US, have any of your favorite cannabis brands gone out of business?